Here’s why you might not get your mortgage-interest deduction.

Here’s why you might not get your mortgage-interest deduction.

According to a report in The Wall Street Journal, some people who have been used to claiming the mortgage interest deduction in the past may not be able to do so going forward.

In fact, new projections from Congress’ Joint Committee on Taxation show that the mortgage interest deduction will be going away for about 18 million of us this year because of certain provisions in the new tax law.

In raw numbers that means only 13.8 million taxpayers are expected to file a 2018 return claiming the mortgage-interest deduction. That’s down from the 32.3 million filers who got the deduction on their 2017 taxes.

To put it another way, the savings from mortgage interest deduction are expected to drop to $25.01 billion on 2018 returns — down from $59.87 billion last year.

Why such a stark change coming? Here’s a look at the specific changes in tax law that will create this situation:

• First, the doubling of the standard deduction to $12,000 for most single filers and $24,000 for most married couples means it may no longer make sense to break out mortgage interest on a Schedule A.

• Second, the new cap on deducting more than $10,000 of state and local income or sales and property taxes (SALT) is per tax return, not per person. Therefore, if you have the maximum SALT deductions of $10,000, you will still need more than an additional $14,000 to make it worth it to file a Schedule A and claim the mortgage interest deduction. If you have anything less than $14,000 in other write-offs — including things like mortgage interest and charity donations — then you won’t get the benefit you’re used to.

• Of course, if you are single, you only need an additional $2,000 in write-offs, assuming you have the max SALT deductions of $10,000. So it’s more likely you’ll get the mortgage deduction than a married couple.

• A third reason you may not be able to claim the mortgage interest deduction going forward is if you made a new home purchase on or after December 15, 2017 and the purchase price was above the new limit of $750,000 for up to two homes.

So, does paying off the mortgage make sense for you?

With the mortgage interest deduction going away for an estimated 18 million taxpayers, it’s safe to say there’s no time like the present to pay off your mortgage — if doing so is within your means.

Now, some people will argue that if you’re borrowing money at very low interest rates — maybe your mortgage rate starts with a “2,” for example — there’s no rush to pay off your mortgage. And there’s certainly a case to be made for that way of thinking when you consider opportunity cost.

In the simplest terms, opportunity costs mean that if you spend tens or hundreds of thousands of dollars paying off your mortgage, you can’t put that money to work in other areas of your life. Effectively, that money won’t be there to grow over the next 10 years, and you’re missing out on some opportunity to build real long-term wealth.

But if your mortgage is your last debt in life, there’s nothing like the peace of mind that comes with being completely debt-free! And once you get that mortgage paid off, you can fully fund your retirement savings every year going forward. So it’s really like six of one or half a dozen of the other, as the saying goes.

“While I am personally a fan of paying off your mortgage early, it’s important to look at the big picture of your current financial situation,” according to Sara Gabrell, a CPA with metro Atlanta tax firm Value Added Inc., who spoke with Clark.com. “There are many factors to take into account before making this type of decision.”

Gabrell says before deciding to pay off your mortgage, ask yourself the following questions:

• Do you have an emergency fund in place?

• Do you have other consumer debt that should be paid off first?

• Are you saving for retirement and fully taking advantage of any employer match on your 401(k)?

Perhaps the most important concern of all is how paying off the mortgage early fits into your long-term financial and wealth building strategies.

“You’ll need your month-to-month budget and finances to be well in order to support that goal over time,” Gabrell advises.

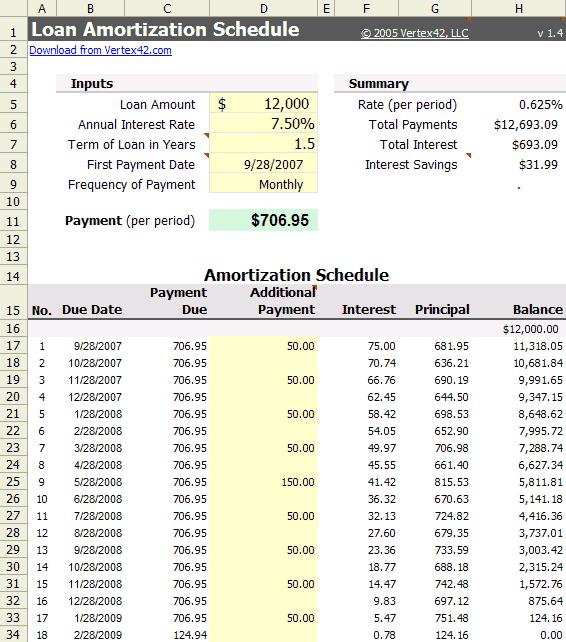

Use an amortization schedule to track your progress

If you still decide a zero mortgage balance should be an immediate goal for you, consider using an amortization schedule as you begin the pay-off process in earnest.

This schedule will help you see the breakdown of how much money goes toward principal and how much money goes toward interest with every mortgage payment you make.

Be forewarned: The numbers aren’t pretty with an amortization schedule. When you first take out a loan, most of your money just gets eaten up by interest and very little goes toward your mortgage’s principal balance!

In fact, looking at an amortization schedule inspired Clark.com writer Mike Timmermann to pay off his $86,000 mortgage in two years.

And if you need more inspiration on your mortgage pay-off journey, we’ve got no shortage of stories about people who buckled down and paid the house note off.

For example, you can read about this couple with three children who paid off their $93,000 mortgage in two years. Or this man who paid off his mortgage and retired when he was just 37 — by putting a 40% downpayment on his home and aggressively paying off the remaining balance over five years.

The point is, there’s no shortage of stories out there about people paying off their mortgage early. Will your story be next?

Originally found here

Picture originally found